The Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 and its companion bill, the Income Tax Rates Amendment (Tax Reform No. 1) Bill 2026, is now officially law.

Introduced with the Income Tax Rates Amendment (Tax Reform No. 1) Bill 2026, the bill amends the:

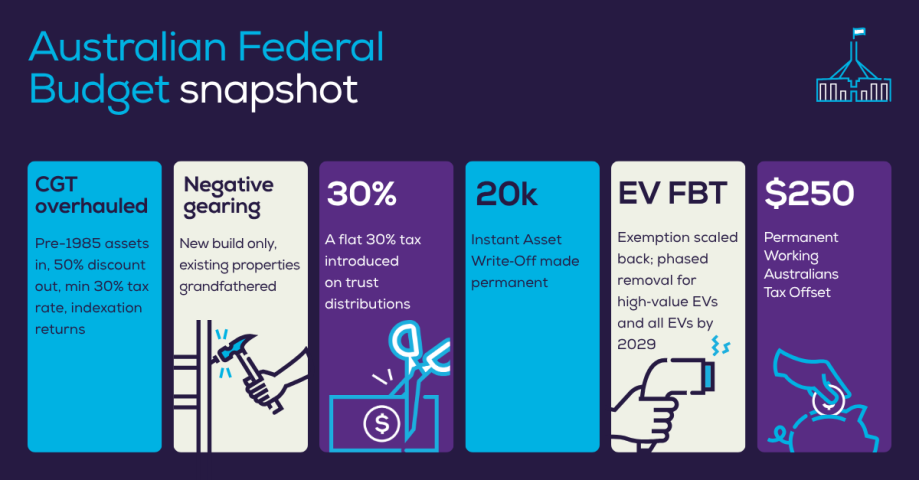

Income Tax Assessment Act 1997 and three other taxation laws to replace the 50 per cent capital gains tax discount for individuals, trusts and partnerships with cost base indexation and a 30 per cent minimum tax rate on capital gains accruing on and after 1 July 2027

Income Tax Assessment Act 1997 to limit negative gearing for residential property investments to new builds from 1 July 2027

Income Tax Assessment Act 1997 to provide for a non-refundable tax offset from the 2027-28 financial year for Australian resident individuals who earn labour income

Income Tax Assessment Act 1997 and Fringe Benefits Tax Assessment Act 1986 to provide for a $1,000 standard deduction from the 2026-27 financial year for work-related expenses for individuals who are Australian tax residents who derive assessable labour income.

Before the Bill passed the Senate, the following changes were made:

Small business CGT discount threshold raised to $10m - small businesses selling active business assets get the 50% CGT discount if their turnover is under $10 million, up from $2 million.

Donations to reduce tax - tax-deductible charitable donations can now reduce the capital gain subject to the new 30% minimum tax.

Limiting ministerial powers - relevant ministers can no longer use their sole discretion to decide what assets qualify for the discount or grant other exemptions. Changes must pass through Parliament.

Super fund property borrowing banned - super funds can no longer take out new loans to buy residential property however any existing arrangements are grandfathered and are unaffected.

For more information or assistance please contact Infinite Accounting Solutions on 02 9899 4730 or via the contact page at www.ias-ca.com.au.

Source: Chartered Accountants ANZ, Parliament of Australia.