The Federal Government delivered the 2026-27 budget on May 12, headlined by a range of major reforms.

IN BRIEF

The conflict in the Middle East has created extreme global volatility and uncertainty, driving up energy costs

Inflation is expected to peak around 5% in June 2026 but forecast to decline to 2.5% by the June quarter 2027, which is back within the RBA's target band of 2-3%.

Unemployment has risen to 4.5%

The government expects a budget deficit of $28.3bn in 2025-26.

KEY POINTS

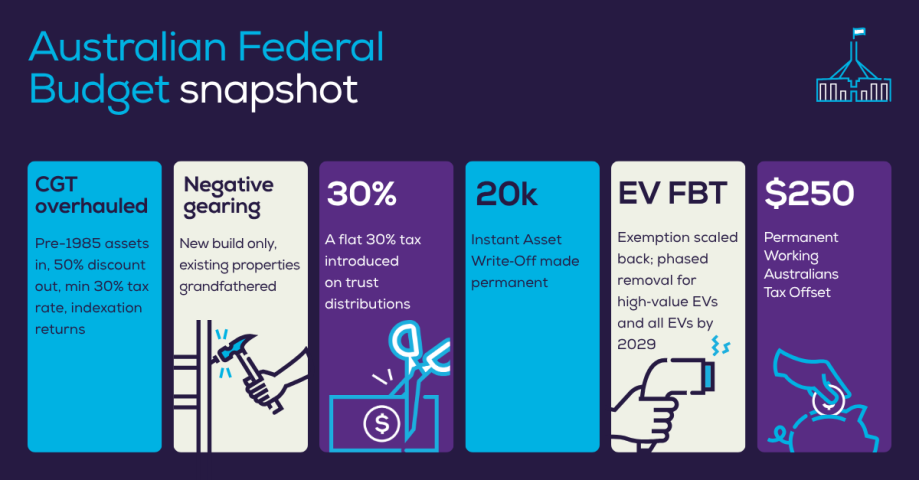

Major reforms

Capital gains tax

From 1 July 2027, a minimum 30% tax on capital gains will be applied after the asset purchase price has been adjusted for inflation. This is instead of the 50% CGT discount as per the current policy.

Trusts

From July 2028, there is a new 30% minimum tax on discretionary trusts which must be paid by the trust itself. After that, beneficiaries receive tax credits for the tax already paid.

Negative gearing

From 1 July 2027, negative gearing can only be claimed on new builds, however, existing investment properties bought before 12 May 2026 are exempt from these new rules.

Personal taxation

$250 working Australians tax offset (WATO)

From 1 July 2027, a new working Australians tax offset (WATO) will be introduced to provide a permanent annual $250 tax offset to all eligible Australian workers for their income derived from work.

Personal tax rates: existing cuts for 2026-27 and 2027-28 unchanged

The Government did not announce any further changes to the personal tax rates.

Standard $1,000 deduction for work-related expenses

This measure – applying to the 2026-2027 income year - allows eligible taxpayers to claim the standard $1,000 deduction for work-related expenses without needing to incur or substantiate these expenses as per the standard deduction.

Medicare levy low-income thresholds for 2025-26

For the 2025-26 income year, the Medicare levy low-income threshold has been increased. For singles it has been increased to $28,011, for couples with no children it has been increased to $47,238 and the additional amount of threshold for each dependent child or student is $4,338.

Private health insurance rebate cut for those aged 65 and over

From 1 April 2027, the private health insurance rebate will be reduced for those aged 65 and over.

Business taxation

Reintroduction of the loss carry-back regime

From 1 July 2026, companies with aggregated annual global turnover of less than $1bn will be able to carry back a tax loss and offset it against tax paid up to 2 years earlier.

Instant asset write-off for small businesses is permanently extended

The $20,000 instant asset write-off for small businesses with a turnover of up to $10m has been permanently extended.

Venture capital tax incentives: asset size caps to be increased

From 1 July 2027, certain asset caps will be increased, including the:

Venture capital limited partnership (VCLP) cap

Early stage venture capital limited partnership (ESVCLP) cap

ESVCLP tax incentive cap

Maximum fund size of ESVCLPs

R&D tax incentive overhaul

From 1 July 2028, reforms to streamline the current R&D program include:

An increase in core R&D offset rates by 4.5% percentage points

Only “core” rather than “supporting” R&D activities can qualify

The turnover threshold for the refundable incentive will rise from $20 million to $50 million aggregated turnover

Refundable offsets will only be available to firms under 10 years old

The R&D intensity threshold will fall from 2% to 1.5% of total business expenditure

The maximum eligible R&D expenditure cap will increase from $150 million to $200 million

The minimum expenditure threshold will rise from $20,000 to $50,000.

Loss refundability for small start-up companies

From 1 July 2028, start-up companies with aggregated annual turnover of less than $10m that generate a tax loss in their first 2 years of operation will be able to utilise the loss to generate a refundable tax offset.

Expansion of dynamic monthly business tax payments

From 1 July 2027, small and medium businesses will be able to opt into reporting and paying PAYG instalments monthly and to using an ATO-approved calculation embedded in accounting software to calculate and vary their instalments.

Fringe Benefits Tax exemption for EVs: full exemption to be phased out; temporary $75,000 threshold proposed

From 1 April 2027, EVs priced above $75,000 but less than the luxury car tax threshold will receive a 25% discount on their payable FBT, rather than the full FBT exemption as per the current scheme.

More funding for ATO: compliance activities and combatting fraud

From 1 July 2026, the ATO will receive $86.3 million over 4 years to counter fraud and modernise the detection and prevention of fraud in tax and super systems.

Improving Australia's business registers

The Government will provide $136.1m over 2 years from 2026-27 to complete the second stage of stabilising Australia's business registers.

Small business debt helpline extended

The Government will provide $8.2m over three years from 2025-26 to extend the Small Business Debt Helpline financial counselling program and the NewAccess for Small Business Owners mental health coaching program to 30 June 2027.

More additions to charities register

Tax law will be amended to list seven more organisations as deductible gift recipients (DGRs).

Superannuation

The Government did not announce any new major super measures.

Other measures

Fuel excise and road user charge temporary reduction

From 1 April to 30 June 2026, the Government temporarily cut the fuel excise on petrol and diesel by 32c. While noted in the Budget, there is no indication that this measure will be extended further beyond the already announced 3-month period.

Eligibility for pension supplement changes

Pension recipients who are residing permanently overseas or who are temporarily absent from Australia for longer than 12 weeks will no longer be eligible for the pension.

Supervision funding for MIS sector

The Government will provide $17.8m over 4 years from 2026-27 (and $1.4m per year ongoing) to strengthen governance requirements, supervision and enforcement in relation to managed investment schemes.

Strengthening child support system

The Government will provide $22m over 4 years from 2026-27 and $600,000 ongoing to various departments including Services Australia, ATO and Department of Social Services to improve the accuracy of child support assessments.

Fighting SMS scams

The Government will introduce a user charge to recover the cost of operating the SMS Sender ID Register from 2026-27.

Rental income help for those receiving Youth Allowance and ABSTUDY

States and Territories will receive $59.4m over 4 years, enabling community housing providers to supplement rental income for over 4,000 young people eligible for social housing.

Increasing withdrawal limit for estate expenses

The Government is increasing the bank account withdrawal limit for deceased persons’ estate related expenses from $15,000 to $30,000, including funeral expenses.

Reducing reporting burden for large proprietary companies

The Government will relieve the reporting burden for large proprietary companies by increasing monetary thresholds from $50m to $100m of consolidated revenue and $25m to $50m of consolidated gross assets. Businesses that don't meet these new thresholds no longer need to lodge an annual audited financial report, directors' report or sustainability report.

The 2026-27 Budget Papers are available from the following website: https://budget.gov.au/

For more information or assistance please contact Infinite Accounting Solutions on 02 9899 4730 or via the contact page at www.ias-ca.com.au

Source : Chartered Accountants ANZ